In the commercial and consumer lending sectors, launching a new loan origination system (LOS) or updating an existing product line is notoriously slow. Enterprise software deployments routinely stretch from an anticipated four-month timeline into a twelve-month saga.

For senior business, tech, and product leaders, these delays carry high stakes. Every month a project stalls is a month of lost revenue, inflated engineering costs, and missed market opportunities. Competitors with more agile frameworks capture market share, while your internal teams remain trapped in deployment cycles.

To accelerate time-to-market, leaders must identify the root causes of implementation friction and adopt a modern approach to deployment architecture.

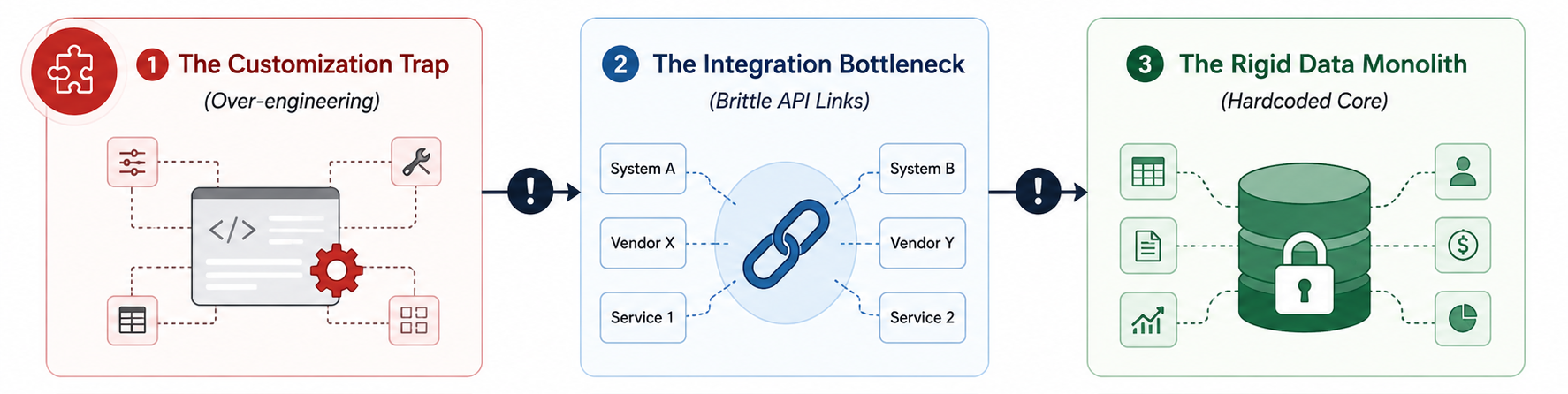

The Three Structural Bottlenecks of Legacy Implementations

Most deployment delays do not stem from a lack of talent or budget. Instead, they are caused by fundamental flaws in how lending technology projects are designed and executed.

1. The Core Customization Trap

Lending institutions often approach a new platform with a long list of highly specific legacy requirements. Instead of adopting standardized, modern workflows, they attempt to rewrite the new software to mirror their old, inefficient manual processes. This leads to massive amounts of custom code, unique edge-case developments, and unforeseen technical debt. The more custom code a platform requires, the longer it takes to build, test, and stabilize.

2. Brittle Integration Ecosystems

A loan origination system cannot operate in a vacuum. It must connect seamlessly to credit bureaus, identity verification services, fraud detection networks, document management systems, and core banking ledgers. In traditional implementations, these connections are built using rigid, point-to-point integrations. If an external vendor updates their API structure, or if the internal team needs to swap out a fraud provider, the entire pipeline breaks, requiring extensive remediation work from engineering teams.

3. Monolithic Architecture and Rigid Data Models

Many traditional systems tie the user interface, the decisioning logic, and the data schema into a single, inseparable monolith. When a product manager wants to change a single field on an application form or add a new data point to the credit assessment process, it requires a full system deployment. This lack of modularity forces teams to move at the speed of their slowest component.

The Blueprint for Accelerated Go-Live

Overcoming these delays requires a structural shift away from monolithic, heavily customized rollouts. Sophisticated lending institutions use a modular, configuration-first strategy to achieve rapid time-to-market.

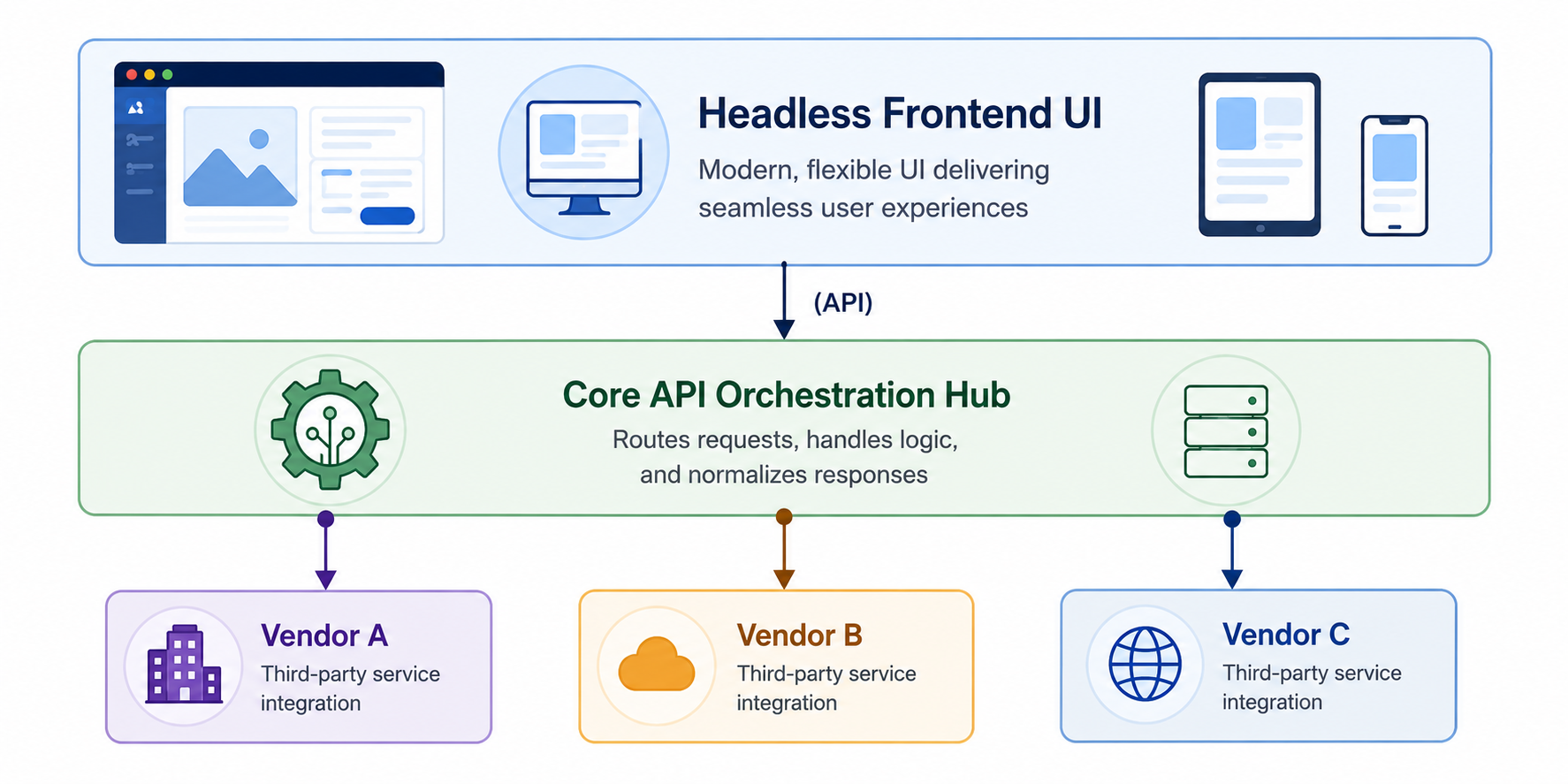

Transition to Composable Architecture

Modern loan origination systems should rely on a composable, headless infrastructure. By separating the front-end user experience from the back-end orchestration layer, product and engineering teams can work concurrently.

The back-end should function as an API orchestration hub. Rather than writing custom code for every vendor integration, teams should use flexible integration layers that abstract data formats into a unified internal schema. This allows the institution to add, remove, or swap third-party data providers in days rather than months.

Prioritize Configuration Over Customization

Senior leaders must champion a configuration-first mindset across product and operations teams. Modern platforms offer visual workflow builders and low-code rules engines that allow risk and product managers to alter credit policies, adjust interest rates, and reorder workflow steps directly.

When business users can make adjustments safely within an administrative interface, the engineering team is freed from handling trivial layout or rule updates. This drastically reduces the development queue and speeds up execution.

Implement a Phased Rollout Strategy

The “Big Bang” approach to software deployment, where an institution attempts to migrate its entire product suite and user base to a new platform on a single day, is highly risky and prone to delays.

A more effective framework is the Minimum Viable Product (MVP) rollout focused on a narrow scope. For example, an institution might launch the new system exclusively for a single, low-risk unsecured loan product in one geographical market. This allows the organization to validate the infrastructure, monitor real-world performance, and iron out operational issues within a controlled environment. Once the baseline platform is proven, migrating subsequent products and portfolios becomes a repeatable process.

Streamlining Internal Governance and Testing

Technology is only half the battle; internal governance models frequently delay project launches. Traditional quality assurance frameworks rely on manual user acceptance testing (UAT) cycles that last for weeks.

To move faster, lending institutions must invest in automated testing frameworks. Automated simulation suites can run thousands of historical credit applications through a new decisioning engine in minutes, instantly highlighting any deviations from expected underwriting outcomes. This gives risk committees immediate, empirical proof that a new system configuration behaves exactly as intended, speeding up internal approvals.

Embracing Agility as a Competitive Advantage

In a lending landscape characterized by shifting regulations and changing consumer expectations, speed to market is a critical metric for success. By abandoning the slow, heavily customized deployment models of the past and adopting a modular, configuration-driven architecture, financial institutions can compress their launch timelines from months to weeks. The result is an organization that responds to market opportunities instantly, optimizes IT spend, and delivers immediate value to both the business and its borrowers.